Table of Contents

Quick Answer

What Is Zero-Based Budgeting in Procurement?

What Is Zero-Based Costing in Manufacturing?

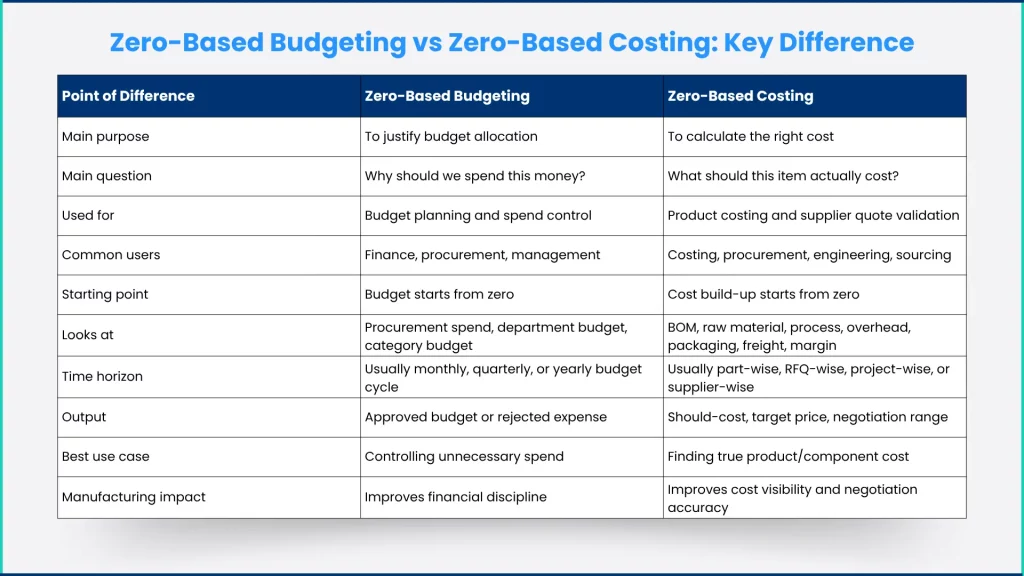

Zero-Based Budgeting vs Zero-Based Costing: Key Difference

Why Manufacturing Teams Confuse Both Terms

Where Zero-Based Budgeting Helps in Manufacturing Procurement

Where Zero-Based Costing Helps in Manufacturing

Zero-Based Budgeting vs Zero-Based Costing vs Should-Cost Analysis

Which One Should Procurement Teams Use?

Common Mistake

Role of Software in Zero-Based Budgeting and Zero-Based Costing

Conclusion

FAQs

Manufacturing companies are under constant pressure to control costs without affecting quality, delivery, or supplier relationships.

Raw material prices change. Supplier quotes vary. Packaging, freight, tooling, overheads, and conversion costs keep adding up. And in many companies, budgets are still created by looking at last year’s numbers and adding a percentage increase.

That is where terms like zero-based budgeting and zero-based costing become important.

But they are not the same.

Zero-based budgeting helps a company decide why money should be spent.

Zero-based costing helps a company understand what a product, component, or process should actually cost.

Both start from zero. Both question old assumptions. Both help reduce unnecessary costs. But in manufacturing, they are used for different decisions.

This blog explains the difference between zero-based budgeting and zero-based costing, how they work in manufacturing, and why procurement and costing teams should use both together.

Quick Answer: Are Zero-Based Budgeting and Zero-Based Costing Different?

Yes, zero-based budgeting and zero-based costing are different.

Zero-based budgeting is a financial planning method where every budget request must be justified from the ground up, instead of using last year’s budget as the base.

Zero-based costing is a cost analysis method where every cost element of a product, part, process, or supplier quote is built from zero to understand what it should actually cost.

In simple words:

Zero-based budgeting justifies the spend. Zero-based costing justifies the cost.

For manufacturing companies, zero-based budgeting is mainly used for procurement budget planning, department-level spend control, and financial discipline. Zero-based costing is used for product costing, should-cost analysis, RFQ comparison, supplier quote validation, and cost negotiation.

What Is Zero-Based Budgeting in Procurement?

Zero-based budgeting, or ZBB, is a budgeting approach where every expense starts from zero and must be justified before it gets approved.

In traditional budgeting, companies often take last year’s procurement budget and increase it based on inflation, expected demand, or business growth. This is easy, but it can carry forward old inefficiencies.

For example, if a company spent ₹10 crore on a procurement category last year, the next year’s budget may become ₹10.8 crore after adding an 8% increase. But this method does not always question whether the original ₹10 crore spend was justified.

Zero-based budgeting changes that.

Instead of asking:

“How much more budget do we need compared to last year?”

It asks:

“What do we actually need to spend, and why?”

In procurement, this means every purchase category, supplier contract, service cost, raw material allocation, logistics expense, and indirect spend item should have a clear business reason.

Example of Zero-Based Budgeting in Procurement

A manufacturing company may review its procurement budget category by category:

- Do we still need this supplier contract?

- Is this purchase linked to current production demand?

- Are we buying more inventory than required?

- Is this service still useful?

- Can this cost be reduced, renegotiated, or removed?

- Does this budget support business priorities?

The goal is not only cost-cutting. The goal is better allocation of money.

What Is Zero-Based Costing in Manufacturing?

Zero-based costing is a costing approach where the cost of a product, part, assembly, process, or supplier quote is built from the ground up.

Instead of accepting the supplier’s quoted price or relying only on past purchase prices, the costing team breaks the cost into individual elements.

In manufacturing, this may include:

- Raw material cost

- Weight or consumption

- Scrap and rejection

- Process cost

- Machine time

- Labour cost

- Power and utilities

- Overhead

- Tooling

- Packaging

- Freight

- Supplier margin

The purpose is to understand what the item should cost, not just what the vendor is quoting.

Example of Zero-Based Costing in Manufacturing

Suppose a supplier quotes ₹520 for a machined component.

Instead of negotiating blindly, the costing team builds the cost from zero:

| Cost Element | Estimated Cost |

|---|---|

| Raw material | ₹210 |

| Machining process | ₹95 |

| Surface treatment | ₹35 |

| Labour | ₹25 |

| Overhead | ₹45 |

| Packaging | ₹15 |

| Freight | ₹10 |

| Supplier margin | ₹35 |

| Should Cost | ₹470 |

Now the procurement team knows that the quoted price of ₹520 may have a negotiation gap of around ₹50.

This makes supplier negotiation more fact-based.

Zero-Based Budgeting vs Zero-Based Costing: Key Difference

The easiest way to understand the difference is this:

Zero-based budgeting is about budget approval. Zero-based costing is about cost accuracy.

Why Manufacturing Teams Confuse Both Terms

Manufacturing teams often confuse zero-based budgeting and zero-based costing because both follow a similar mindset.

Both ask teams to stop relying blindly on the past.

Traditional budgeting often says:

“We spent this much last year, so this year we need slightly more.”

Traditional costing or negotiation often says:

“This supplier quoted this much last time, so let us negotiate from there.”

Both approaches can create cost leakage.

Zero-based budgeting and zero-based costing push teams to rebuild the logic from zero.

But the application is different.

Zero-based budgeting works at the spend and budget level.

Zero-based costing works at the product and cost-driver level.

Manufacturing Example: How Both Work Together

Let’s take a simple example.

A company manufactures an automotive assembly and needs to prepare next quarter’s procurement budget. The procurement budget includes raw materials, purchased parts, packaging, freight, consumables, tooling, and supplier services.

Step 1: Zero-Based Budgeting View

The finance and procurement teams first ask:

- What components are actually required for production?

- What quantity is needed based on demand?

- Which supplier contracts are still active and necessary?

- Which purchase categories can be optimized?

- Which costs are essential and which are avoidable?

This helps the company decide how much procurement budget should be approved.

Step 2: Zero-Based Costing View

Once the budget category is approved, the costing and procurement teams go deeper.

For each major component, they ask:

- What is the raw material requirement?

- What is the current material rate?

- What process is required?

- How much machine time is needed?

- What is the fair conversion cost?

- Is the supplier adding too much overhead?

- Is packaging charged separately or hidden inside the quote?

- Is freight realistic?

- What should be the target price?

This helps the company decide whether the quoted price is fair.

Final Output

Zero-based budgeting helps answer:

“Should we allocate budget for this purchase?”

Zero-based costing helps answer:

“What should we pay for this purchase?”

Together, they give procurement teams better control over both budget and cost.

Where Zero-Based Budgeting Helps in Manufacturing Procurement

Zero-based budgeting is useful when a manufacturing company wants better control over procurement spend.

It helps in areas like:

1. Procurement Budget Planning

Instead of approving spending based on past numbers, teams review every category based on current production needs, demand plans, and business priorities.

2. Indirect Spend Control

Indirect procurement often carries hidden waste. Items like consumables, office supplies, maintenance services, subscriptions, and non-production purchases may continue without proper review. ZBB helps question these costs.

3. Supplier Contract Review

Some supplier contracts continue for years without fresh evaluation. Zero-based budgeting helps procurement teams check whether a contract is still needed, competitive, and aligned with current requirements.

4. Better Cost Accountability

Every department or function needs to explain why a budget is required. This improves ownership and reduces unnecessary approvals.

5. Spend Prioritization

When budgets are limited, zero-based budgeting helps companies prioritize critical spend over low-value expenses.

Where Zero-Based Costing Helps in Manufacturing

Zero-based costing is useful when a company wants better visibility into the actual cost of a product, part, or supplier quote.

It helps in areas like:

1. Should-Cost Analysis

Zero-based costing is closely connected with should-cost analysis. It builds the expected cost of a product from cost drivers instead of relying only on vendor quotes.

2. RFQ Comparison

In RFQs, different suppliers may quote different prices with different assumptions. One quote may include packaging, another may exclude freight, and another may include only raw material and process cost.

Zero-based costing helps normalize these quotes and compare them fairly.

3. Supplier Negotiation

Procurement teams can negotiate better when they know the cost breakdown. Instead of asking for a random discount, they can question specific cost drivers.

For example:

- Why is material cost higher than market benchmark?

- Why is process cost inflated?

- Is packaging charged twice?

- Is overhead too high?

- Is freight included correctly?

4. Product Cost Reduction

Zero-based costing helps identify which cost element is driving the final price. This can lead to design changes, alternate materials, process optimization, supplier change, or packaging improvement.

5. Cost Leakage Detection

Cost leakage often hides inside small assumptions: extra scrap, outdated material rates, high overhead, duplicate packaging, wrong freight, or incomplete quote comparison. Zero-based costing helps expose these gaps.

Zero-Based Budgeting vs Zero-Based Costing vs Should-Cost Analysis

These three terms are connected, but they are not identical.

| Concept | Meaning | Manufacturing Use |

| Zero-Based Budgeting | Every budget request starts from zero and must be justified | Procurement budget control |

| Zero-Based Costing | Every cost element is built from zero | Product or component cost build-up |

| Should-Cost Analysis | Estimating what a product should cost based on materials, process, overhead, and margin | Supplier quote validation and negotiation |

A simple way to look at it:

- Zero-based budgeting decides whether the spend is required.

- Zero-based costing calculates the correct cost structure.

- Should-cost analysis turns that cost structure into a negotiation baseline.

For manufacturing procurement, this combination is very powerful.

Which One Should Procurement Teams Use?

Procurement teams should use both, but for different decisions.

Use zero-based budgeting when you are planning or approving spend.

Use zero-based costing when you are evaluating a product cost, supplier quote, or RFQ.

| Situation | Better Approach |

| Preparing annual procurement budget | Zero-Based Budgeting |

| Reviewing whether a purchase is necessary | Zero-Based Budgeting |

| Validating a supplier quotation | Zero-Based Costing |

| Comparing RFQ responses | Zero-Based Costing |

| Setting a target price | Zero-Based Costing / Should-Cost Analysis |

| Reducing indirect procurement waste | Zero-Based Budgeting |

| Finding hidden cost drivers in a component | Zero-Based Costing |

| Improving negotiation with suppliers | Zero-Based Costing |

| Controlling total procurement spend | Both |

Common Mistake: Using Budgeting Without Costing

One common mistake in manufacturing procurement is trying to control budgets without understanding cost drivers.

A company may reduce the procurement budget by 5%, but if the team does not understand the cost structure, the reduction may happen in the wrong area.

For example, reducing supplier price without understanding material cost, conversion cost, or quality requirements can lead to:

- poor quality

- supplier resistance

- delayed delivery

- hidden charges

- later cost escalation

- lower product reliability

That is why zero-based budgeting should not be used only as a cost-cutting exercise.

It should be supported by zero-based costing and should-cost analysis.

Budget control without cost visibility can become dangerous.

Cost visibility makes budget control smarter.

Common Mistake: Using Costing Without Budget Discipline

The opposite problem also happens.

Some companies do detailed product costing but still approve budgets based on old patterns.

In this case, even if the costing team finds savings opportunities, the business may still carry forward unnecessary spend in other areas.

For example:

- old supplier contracts continue

- low-value purchases remain active

- indirect procurement is not reviewed

- outdated tooling costs stay in the system

- duplicate services continue

- budgets increase automatically every year

This is where zero-based budgeting adds value.

It creates a discipline where every spend must be reviewed, justified, and connected to business value.

Role of Software in Zero-Based Budgeting and Zero-Based Costing

Both zero-based budgeting and zero-based costing become difficult when data is scattered across Excel files, emails, ERP exports, supplier quotations, and manual approvals.

Manufacturing teams need connected data to make both approaches work properly.

For zero-based budgeting, software can help teams:

- track procurement spend category-wise

- compare planned vs actual spend

- review supplier contracts

- manage approvals

- identify unnecessary expenses

- create budget visibility across departments

For zero-based costing, software can help teams:

- build cost breakdowns

- calculate should-cost

- compare supplier quotes

- analyze RFQ responses

- detect anomalies in cost data

- simulate cost impact at product level

- create negotiation baselines

This is where manufacturing cost intelligence becomes important.

When procurement, costing, RFQ, supplier data, and approval workflows are connected, teams can move from reactive cost control to proactive cost decision-making.

Conclusion

Zero-based budgeting and zero-based costing both help manufacturing companies improve cost control, but they work at different levels.

Zero-based budgeting helps procurement and finance teams decide whether a spend should be approved.

Zero-based costing helps costing and procurement teams understand what a product, component, or supplier quote should actually cost.

One controls the budget. The other controls the cost logic.

For manufacturing companies, using only one of them is not enough. Budgeting without costing can lead to blind cost cuts. Costing without budgeting can leave unnecessary spend untouched.

The real value comes when both are connected.

That is how procurement teams can reduce cost leakage, improve RFQ decisions, negotiate with suppliers more confidently, and make better cost decisions before money is spent.

If your procurement and costing teams are still managing budgets, RFQs, and supplier cost analysis through scattered spreadsheets, it becomes difficult to see where the real cost leakage is happening.

Cost it Right helps manufacturing teams connect costing, procurement, RFQ, supplier comparison, and cost simulation in one platform, so teams can make better cost decisions with clearer visibility.

FAQs

No. Zero-based budgeting is used to justify budget allocation, while zero-based costing is used to calculate the expected cost of a product, part, or process from the ground up.

Zero-based budgeting in procurement is a method where every procurement expense must be justified from zero instead of being approved based on last year’s spend. It helps reduce unnecessary purchases and improves budget discipline.

Zero-based costing in manufacturing is a method of building the cost of a product or component from individual cost elements such as raw material, process, labour, overhead, packaging, freight, and supplier margin.

Zero-based costing gives procurement teams a cost breakdown. This helps them negotiate specific cost drivers instead of asking suppliers for random discounts.

Zero-based budgeting helps manufacturing companies control procurement spend, remove unnecessary costs, review supplier contracts, and allocate budgets based on current business needs.

Zero-based costing helps procurement teams compare supplier quotes on the same cost basis. It can identify missing cost elements, inflated charges, and incomplete supplier submissions.

Neither is better. They solve different problems. Zero-based budgeting is better for budget control, while zero-based costing is better for product cost analysis and supplier quote validation.

Yes. In manufacturing procurement, they work best together. Zero-based budgeting controls where money is spent, while zero-based costing ensures the amount paid is fair and justified.