Quick Answer

Should-cost analysis is done by breaking down the expected cost of a product into its major cost components, such as raw material, process cost, labor, overhead, packaging, freight, tooling, rejection, and supplier margin.

To do should-cost analysis step by step, manufacturers need to understand the product, identify cost drivers, collect cost inputs, build a cost model, compare it with supplier quotes, find gaps, and use the analysis for negotiation and decision-making.

The goal is simple: know what a product should cost before accepting what a supplier says it costs.

What Is Should-Cost Analysis?

Should-cost analysis is the process of estimating what a product, part, or assembly should ideally cost based on its material, process, labor, overhead, logistics, and supplier margin.

In procurement, should-cost analysis helps teams evaluate whether a supplier quote is reasonable.

It answers questions like:

- What should this part actually cost?

- Which cost element is inflated?

- Is the supplier quote complete?

- Where is the negotiation opportunity?

- Is the lowest quote really the best option?

Should-cost analysis is not just a costing exercise. It is a decision-making tool.

For a broader understanding of product-level costing, you can also read our detailed guide on should-cost analysis for product cost.

Why Should-Cost Analysis Matters in Procurement

Should-cost analysis helps procurement teams move from opinion-based negotiation to data-backed negotiation.

Without should-cost analysis, teams often depend on:

- supplier quotes

- past purchase prices

- manual assumptions

- Excel-based comparisons

- incomplete benchmarks

However, with should-cost analysis, teams can evaluate supplier quotes using a structured cost model.

This improves:

- supplier negotiation

- RFQ comparison

- cost visibility

- vendor selection

- margin control

- procurement cost reduction

More importantly, it helps prevent cost leakage before the purchase decision is approved.

To understand how this connects with sourcing and supplier evaluation, read our blog on should-cost analysis in procurement.

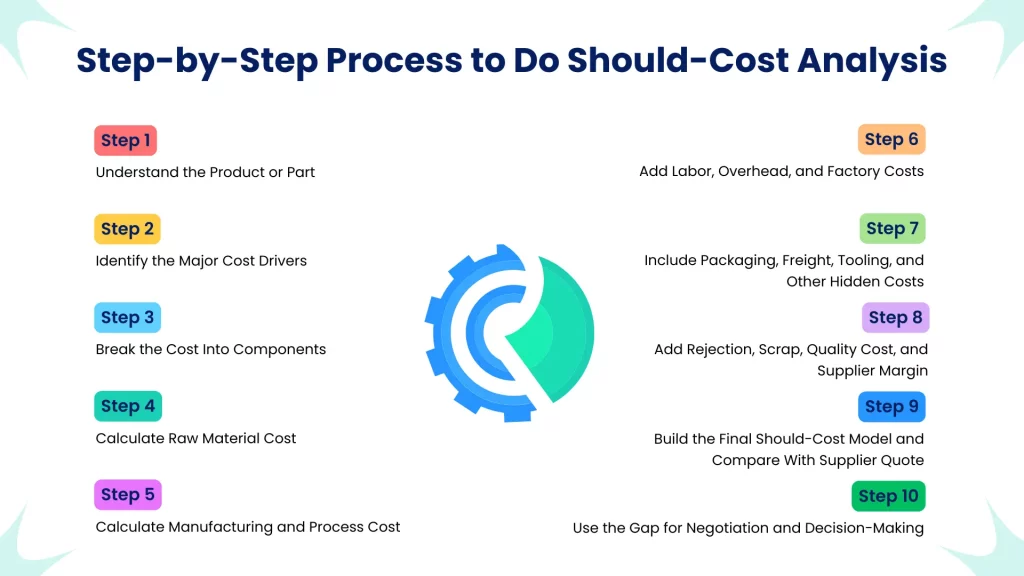

Step-by-Step Process to Do Should-Cost Analysis

Step 1: Understand the Product or Part

Start by collecting the basic product details.

This includes:

- part name

- part number

- drawing or specification

- material grade

- dimensions

- weight

- manufacturing process

- annual volume

- quality requirements

- packaging requirements

- delivery location

This step is important because cost changes based on design, material, volume, process complexity, and supplier capability.

Step 2: Identify the Major Cost Drivers

Once the product is understood, identify the elements that directly influence the final cost.

Common cost drivers include:

- raw material

- weight

- scrap rate

- machine cycle time

- labor time

- process complexity

- tooling requirement

- batch size

- rejection rate

- packaging

- freight

- supplier margin

In many cases, one or two cost drivers explain most of the price difference between suppliers.

Step 3: Break the Cost Into Components

A proper should-cost analysis should show a cost breakdown, not just one final number.

| Cost Component | What It Covers |

|---|---|

| Raw Material | Base material cost based on grade, weight, and market rate |

| Process Cost | Machining, molding, stamping, assembly, or other operations |

| Labor Cost | Direct manpower required for production |

| Overhead | Factory overhead, utilities, maintenance, supervision |

| Tooling | Dies, molds, fixtures, or special tools |

| Packaging | Boxes, pallets, crates, bins, or special packaging |

| Freight | Transportation and logistics cost |

| Rejection/Scrap | Cost impact of expected rejection or scrap |

| Supplier Margin | Profit margin added by supplier |

This breakdown helps procurement teams see where the supplier quote is reasonable and where it needs to be challenged.

Step 4: Calculate Raw Material Cost

Raw material is often one of the largest cost elements in manufacturing.

To calculate it, consider:

- material type

- material grade

- gross weight

- net weight

- scrap percentage

- raw material rate

- yield or utilization factor

A simple formula is:

Raw Material Cost = Gross Material Required × Material Rate

For example, if a component needs 2 kg of material and the material rate is ₹120 per kg:

Raw Material Cost = 2 × 120 = ₹240

If scrap or yield loss is involved, that should also be included.

Step 5: Calculate Manufacturing and Process Cost

Process cost depends on the operations needed to produce the part.

This may include:

- cutting

- stamping

- machining

- welding

- molding

- painting

- heat treatment

- assembly

- surface treatment

To estimate process cost, consider:

- machine hourly rate

- cycle time

- setup time

- labor requirement

- batch size

- energy consumption

- process complexity

A simple formula is:

Process Cost = Machine Hour Rate × Time Required

For example, if machine rate is ₹900 per hour and the part takes 6 minutes:

6 minutes = 0.1 hour

Process Cost = 900 × 0.1 = ₹90

Step 6: Add Labor, Overhead, and Factory Costs

After raw material and process cost, add the supporting costs required to manufacture the product.

This includes:

- direct labor

- supervision

- electricity

- maintenance

- quality control

- administration

- depreciation

- factory overhead

Labor cost can be calculated using:

Labor Cost = Labor Rate × Labor Time

Overhead may be added as a percentage of direct cost or calculated based on machine/process rates.

The key is to make these costs visible instead of accepting them as a flat supplier markup.

Step 7: Include Packaging, Freight, Tooling, and Other Hidden Costs

Many should-cost models fail because they miss indirect or one-time cost elements.

Include:

- packaging

- freight

- handling

- loading/unloading

- insurance

- duties or taxes

- tooling

- dies

- molds

- jigs

- fixtures

- gauges

For tooling, use amortization if required.

For example:

If tooling cost is ₹5,00,000 and expected production volume is 1,00,000 parts:

Tooling Cost per Part = 5,00,000 / 1,00,000 = ₹5 per part

This makes supplier comparison more accurate.

Step 8: Add Rejection, Scrap, Quality Cost, and Supplier Margin

Quality-related costs can change the real cost of a supplier decision.

Include:

- expected rejection rate

- scrap cost

- rework cost

- inspection cost

- warranty risk

- quality failure impact

After that, add a reasonable supplier margin based on:

- product complexity

- supplier capability

- production volume

- market conditions

- risk

- investment required

The goal is not to remove supplier profit. The goal is to understand whether the quote is fair, inflated, incomplete, or negotiable.

Step 9: Build the Final Should-Cost Model and Compare With Supplier Quote

Once all cost elements are calculated, combine them into one model.

Example:

| Cost Element | Value |

|---|---|

| Raw Material | ₹240 |

| Process Cost | ₹90 |

| Labor + Overhead | ₹85 |

| Packaging + Freight | ₹35 |

| Tooling Amortization | ₹5 |

| Rejection/Scrap | ₹10 |

| Supplier Margin | ₹40 |

| Total Should-Cost | ₹505 |

Now, if the supplier quote is ₹620, the gap is ₹115.

This gap becomes the basis for negotiation.

Look for:

- inflated cost elements

- missing cost heads

- abnormal margins

- excessive packaging or freight

- unclear tooling charges

- unrealistic low pricing

A quote can be risky if it is too high, but it can also be risky if it is too low and missing key cost elements.

Step 10: Use the Gap for Negotiation and Decision-Making

The final step is to use the should-cost analysis in real procurement decisions.

Instead of saying:

“Your price is high.”

The buyer can say:

“Your process cost is 18% higher than our benchmark. Can you explain the cycle time or machine rate used?”

This makes negotiation specific, professional, and evidence-based.

Should-cost analysis should support:

- RFQ comparison

- supplier selection

- cost approval

- vendor negotiation

- cost reduction

- product pricing

- margin protection

- make-vs-buy decisions

It should not remain as a separate costing file. It should become part of the procurement workflow.

Should-Cost Analysis vs Cost-Benefit Analysis

Should-cost analysis and cost-benefit analysis are related, but they are not the same.

Should-cost analysis focuses on estimating what a product, part, or supplier quote should cost. It is mainly used in procurement, RFQ comparison, supplier negotiation, and cost control.

Cost-benefit analysis, also called benefit-cost analysis, compares the expected benefits of a decision against its costs. It is usually used to evaluate whether a project, investment, or business decision is worth pursuing.

| Method | Main Purpose | Used For |

|---|---|---|

| Should-Cost Analysis | Estimate the fair cost of a product or supplier quote | Procurement, costing, RFQ, supplier negotiation |

| Budgeting, procurement, and manufacturing cost control | Compare cost against expected business benefit | Investment decisions, project approval, business cases |

| Cost Analysis | Understand where costs come from | Budgeting, procurement, manufacturing cost control |

For manufacturers, should-cost analysis is more useful when the goal is to evaluate supplier pricing, identify cost gaps, and negotiate with better cost visibility.

Common Mistakes in Should-Cost Analysis

Even when teams use should-cost analysis, mistakes can happen.

Common mistakes include:

- using outdated material rates

- ignoring freight and packaging

- not including tooling amortization

- using an incorrect process cycle time

- missing rejection or scrap cost

- Comparing should-cost with incomplete supplier quotes

- not updating the model when assumptions change

- Treating should-cost as a fixed number instead of a decision benchmark

A good should-cost model should be updated regularly.

It should reflect current material rates, supplier conditions, process assumptions, and volume changes.

How AI Helps in Should-Cost Analysis

AI can make should-cost analysis faster and more accurate.

AI can help teams:

extract cost data from PDFs, drawings, emails, and spreadsheets

standardize cost inputs

identify missing cost elements

compare supplier quotes with should-cost models

detect anomalies in pricing

update benchmarks faster

simulate cost impact

generate negotiation insights

However, AI works best when the underlying data is clean and connected.

If the data is scattered, AI may only speed up confusion.

That is why connected costing and procurement data are important.

Role of Cost It Right in Should-Cost Analysis

Platforms like Cost It Right help manufacturers build structured should-cost models, compare supplier quotes, analyze RFQs, track cost drivers, and simulate cost impact before decisions are approved.

This helps procurement and costing teams move from manual comparison to data-driven decision-making.

Instead of relying only on supplier quotes, teams can evaluate whether the quoted price is fair, complete, and aligned with the expected cost.

Conclusion

Should-cost analysis is one of the most important tools for procurement and costing teams.

It helps manufacturers understand what a product should cost before accepting supplier pricing.

When done properly, should-cost analysis improves supplier negotiation, RFQ comparison, cost visibility, and margin control.

The process is simple:

Understand the product.

Break down the cost.

Build the model.

Compare supplier quotes.

Identify gaps.

Negotiate with data.

Use the result for better decisions.

Procurement without should-cost analysis is guesswork.

Procurement with should-cost analysis is controlled decision-making.

FAQ

To perform should-cost analysis, understand the product, identify cost drivers, calculate material and process costs, add overhead, packaging, freight, tooling, rejection, and supplier margin, then compare the result with supplier quotes.

Should-cost analysis is the process of estimating the ideal cost of a product based on material, process, labor, overhead, logistics, and supplier margin.

To do should-cost analysis step by step, collect product data, identify cost drivers, break down cost components, calculate each cost element, build the final model, compare it with supplier quotes, and use the gap for negotiation.

A should-cost analysis example may include raw material, process cost, labor, overhead, packaging, freight, tooling, rejection, and supplier margin. If the total should-cost is ₹505 and the supplier quote is ₹620, the ₹115 difference becomes a negotiation opportunity.

It helps procurement teams evaluate supplier quotes, identify inflated costs, negotiate better, and reduce procurement cost leakage.

A should-cost model should include raw material, process cost, labor, overhead, packaging, freight, tooling, rejection, scrap, and supplier margin.

No. Should-cost analysis estimates the fair cost of a product or supplier quote. Cost-benefit analysis compares the expected benefits of a decision against its total cost.